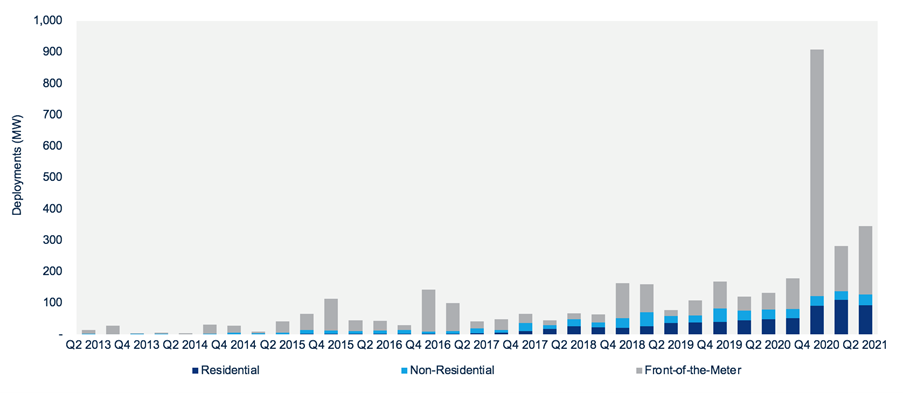

According to Wood Mackenzie, a Verisk business, and the U.S. Energy Storage Association’s (ESA) latest “U.S. Energy Storage Monitor” report, 345 MW of new energy storage systems were brought online in the second quarter of 2021.

Quarterly growth in the U.S. storage market

This is an increase of 162% over the same quarter in 2020, making Q2 2021 the second-largest quarter on record by megawatt for U.S. energy storage additions. Market momentum continues to build, as an unprecedented volume of storage will come online in in the second half of the year, with Wood Mackenzie expecting that storage projects representing over $5 billion of investment will come online in 2021 alone.

Despite positive market momentum in the United States, the residential battery market dipped slightly, the first drop for the segment in nine quarters (since Q4 2018). Equipment constraints, including an ongoing Tesla Powerwall shortage, is hampering the segment’s growth despite the proliferation of new residential storage players.

The non-residential segment, which consists of onsite storage and community-scale storage, saw quarter-on-quarter deployments rise by 31%, driven by the growth of the community storage market in Massachusetts.

The Saticoy battery energy storage system in Ventura County.

The front-of-the-meter (FTM) market deployed 218 MW/729 MWh in Q2 2021, with California, Texas and Arizona leading the segment. California continued to lead the FTM segment in Q2, with Arevon/Capital Dynamics’s 100-MW/400-MWh Saticoy Energy Storage peaker plant replacement in Ventura County contributing most of the megawatts for the quarter. Solar + storage projects in Texas and Arizona also bolstered Q2 FTM capacity.

“The United States remains on course for a record-setting year, further demonstrating battery storage’s growing acceptance within the power market and underlining its importance to the energy transition,” said Vanessa Witte, senior energy storage analyst with Wood Mackenzie.

“While the market for energy storage in the U.S. has seen tremendous growth this year, public policy has yet to support the pace of deployment needed to meet decarbonization and resilience goals,” said Jason Burwen, U.S. Energy Storage Association Interim CEO. “An investment tax credit, which catapulted industries like solar and wind, can do the same for the energy storage industry — with the added benefit of steering more supply chain investment decisions onshore.”

Policy support continued to build in the second quarter, with several new state incentives introduced for residential and non-residential storage. The industry also still awaits the outcome of budget reconciliation, expected this winter, which could include a solar investment tac credit (ITC) extension and/or standalone storage ITC. A positive outcome would upgrade the energy forecast across all segments.

News item from ESA

“Despite positive market momentum in the United States, the residential battery market dipped slightly, the first drop for the segment in nine quarters (since Q4 2018). Equipment constraints, including an ongoing Tesla Powerwall shortage, is hampering the segment’s growth despite the proliferation of new residential storage players.”

The problem is name recognition of TESLA, TESLA, TESLA and not some less well known names in the ESS market. A couple of years ago a relatively solid residential ESS company Pika Energy was absorbed by GENERAC a relatively well known name in the backup generator business. Announced here ESS company and panel builder Simpliphi has been purchased by Briggs and Stratton, better known for gardening equipment and somewhat known for small generator systems. There are smaller startups with very good engineering and equipment like Humless Universal, Sonnen is fairly well known in residential ESS sectors and it too was bought out by Shell Oil a few years back. With just California alone and the quick construction of smart ESS around the State by many entities, utilities, C&I entities are beginning to “soak up” millions of battery cells and thousands of battery packs for distributed energy storage in the State. Now there seem to be more Micro-grid oriented ESS units like ELM Fieldsight 2030 series of ESS for larger homes and perhaps medium businesses. The giga factories keep coming online and battery manufacturing will rise in the next several years World wide. The hope and promise here is that large scale demand will push manufacturing output to levels that will allow residential solar PV and ESS to become the go to system for installation on homes and small businesses from now on. Getting smart ESS technology away from $1,000/kWh to around $300 to $350/kWh installed would make a nice effective energy system to use in one’s home for energy use and resiliency.

The historical relevance should not be ignored, in the year 2000 a (subsidized) simple grid tied solar PV system was around $8 to $9/watt installed would have bought you a 4.5kWp to 5kWp solar PV system for about $40K. Right now one can get some 10kWp and a smart ESS in the 20kWh storage range for the same $40K without the ITC. The mandate of decarbonization of the grid by 2035 implies that some kind of ITC will continue on for some years to come. It has been proposed that the 30% ITC be reinstated and would ramp down and stop at 25% until Congress deems it not necessary anymore. We shall see what the cost of adoption will truly be over the next say 10 years.