Due to the increased global solar installation demand (IHS expects it to reach 65.5 GW this year), demand for modules will also grow. Module shipments will exceed 2015 numbers by 10%, according to IHS, with revenues hitting $41.9 billion. Demand and supply restrictions to the United States because of anti-dumping trade disputes will prevent prices from falling until the end of 2016.

PV Pricing Forecast (Industry average module price, Chinese producer)

Source: GTM Research PV Pulse, March 2016

GTM Research found that the average price of tier-1 Chinese-produced modules reached 57 cents per watt at the end of 2015. The group also predicts that global prices will fall at an annual rate of 5% and reach 44 cents per watt by 2020.

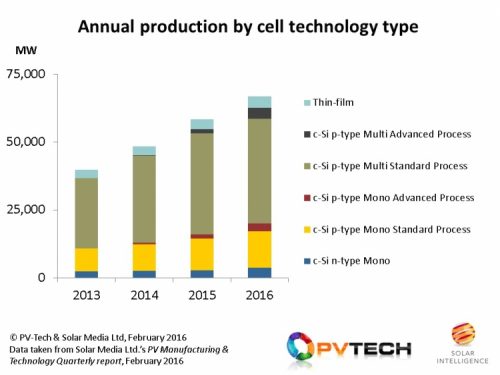

The uptick in demand is reflected on production lines for all cell technology types. PV-Tech research shows that standard c-Si p-type modules will still have market dominance, but no technology type is growing at a significant rate over last year. And while n-type cells have received press coverage over the last year, they are not as market-mainstream as imagined—but check back in a few years.

Annual product by cell technology type

Source: PV-Tech and Solar Media Ltd. PV Manufacturing & Technology Quarterly report, Feb. 2016

All technology types will stay consistent with their market shares over the next year, but Boviet Solar USA CEO Eric Ma believes monocrystalline will eventually pull ahead in the near future.

“I think we’ll see monocrystalline technology gain traction and market share again due to the implementation of cost reduction measures within mono cell and wafer production,” he said. “I think mono and poly costs will be nearly on par within a couple of years, and I expect to see more mono in utility-scale applications as a result of that coupled with its efficiency advantages.”

Tell Us What You Think!